Created for investors to access the diversification benefits of a formally exclusive, often expensive, but compelling asset class. This Index-Plus, low cost and diversified solution delivers efficient exposure to the managed futures space.

What are managed futures?

An investment strategy that seeks trends across commodity, rates, currency, and equity markets.

Managed

Dynamic and tactical approach, not static

Futures

Takes long and short positions using futures contracts

Quant

Humans build models, models determine portfolios

Trends

Durable source of alpha based on prices, not macro calls

What can managed futures do for your portfolio?

An incredibly valuable portfolio diversifier to stocks and bonds

Long-term returns

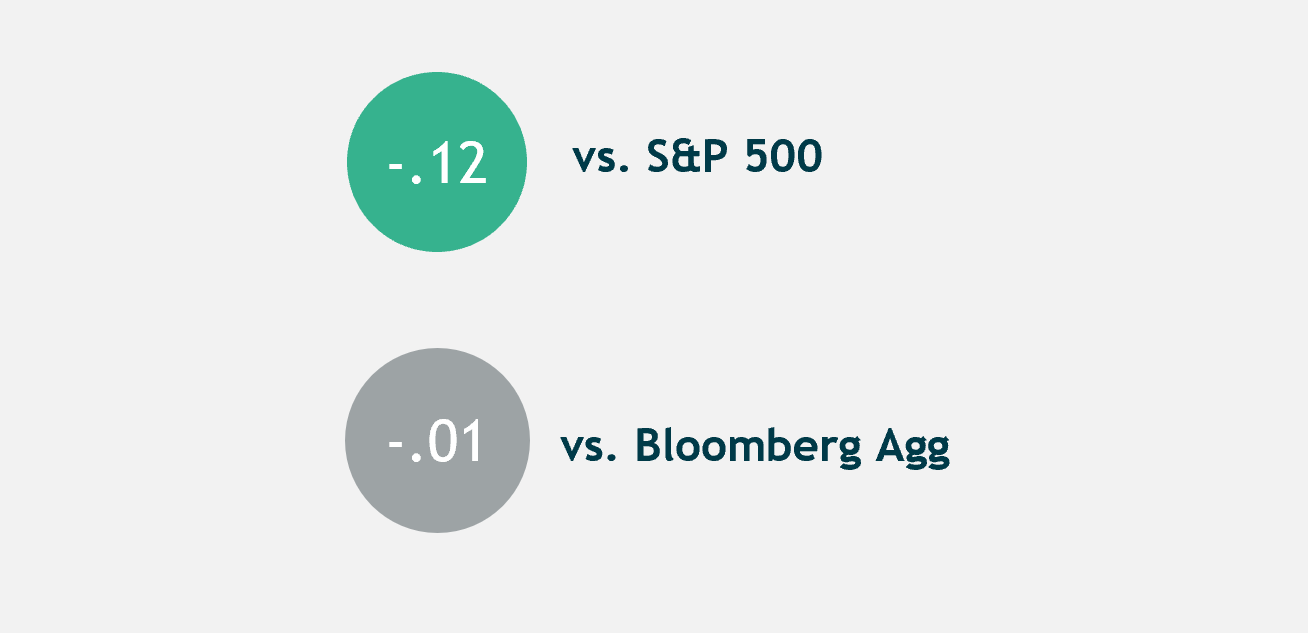

Low correlation to traditional asset classes

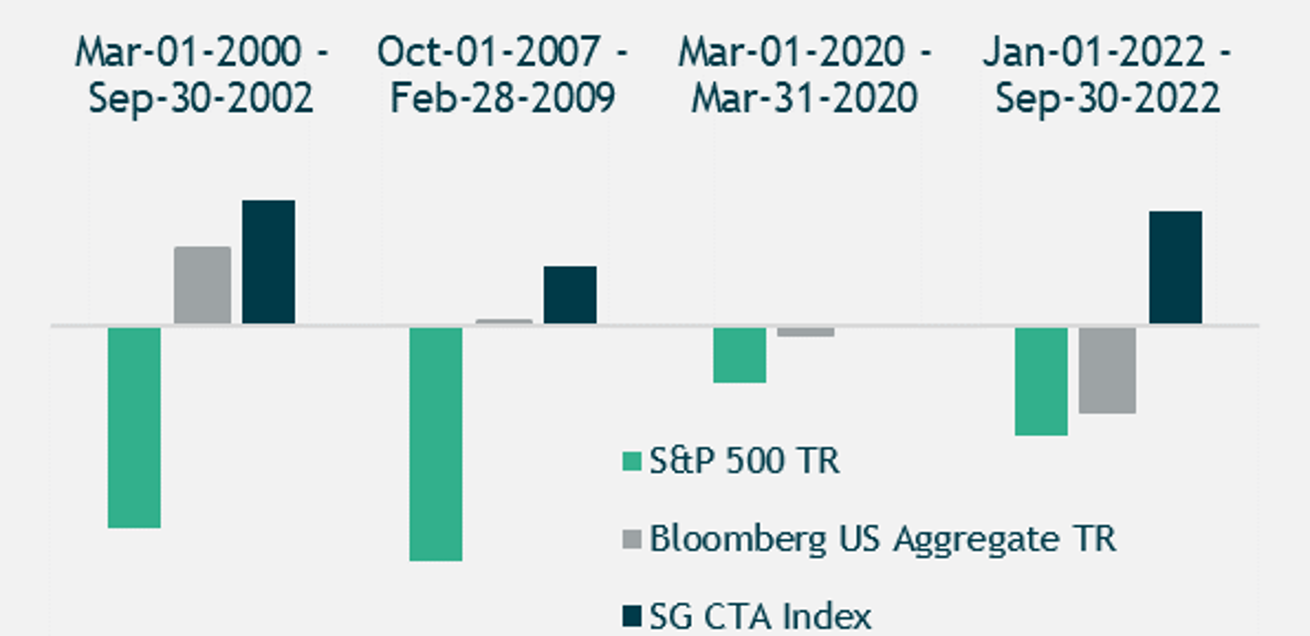

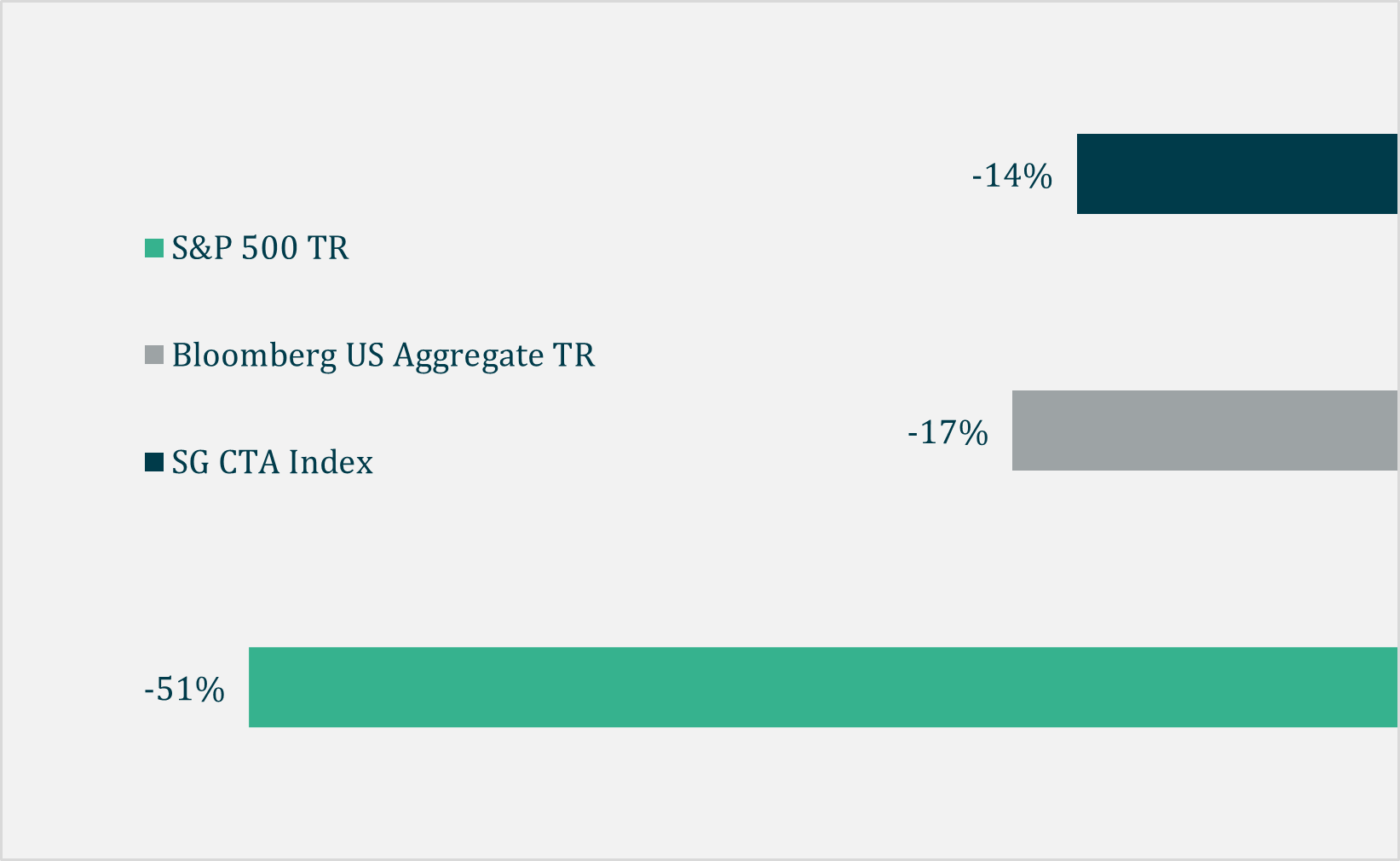

Alpha during prolonged crises

Max drawdown significantly lower than traditional asset classes

The Case for Managed Futures

Explore how to build a durable strategy using managed futures.

DownloadQuestions on Managed futures Allocations

Get insightsThe Great Diversifier: Managed Futures & DBMF Webinar Replay

WatchWhy Managed futures are ripe for replication

ReadFrequently asked questions

Get answers to your questions from our portfolio managers

But the allocation can’t be so big that you (or your client) will throw in the towel during rough patches. The best asset allocation is one that you can stick to for the long term, including through down periods for every component asset class or strategy. Every situation is different, but we think an allocation to managed futures in the 5% to 10% range is the practical sweet spot for most balanced portfolio investors (although higher allocations are well supported by the statistics).

A reasonable case could also be made to fund an allocation more than pro rata from bonds, given stocks outperform bonds over long time horizons, and managed futures tend to perform well during extended stock market weakness (i.e., periods of weeks to months, not days to weeks). The “optimal” allocation depends on what is being optimized (risk-adjusted returns, expected maximum total return, etc.). For a client that is more concerned with risk from a specific asset class, or has some other consideration, the funding sources could of course be customized further according to individual circumstances.

While the details and execution are complex, the underlying premise is simple: across equity markets, bond markets, commodities and currencies, go long assets/markets that are rising in price, and go short assets/markets that are falling in price, using liquid futures contracts to gain exposure. There are numerous theories addressing why trend following works, including divergent economic fundamentals across countries and industries, supply-demand dynamics, market structure, and investor psychology.

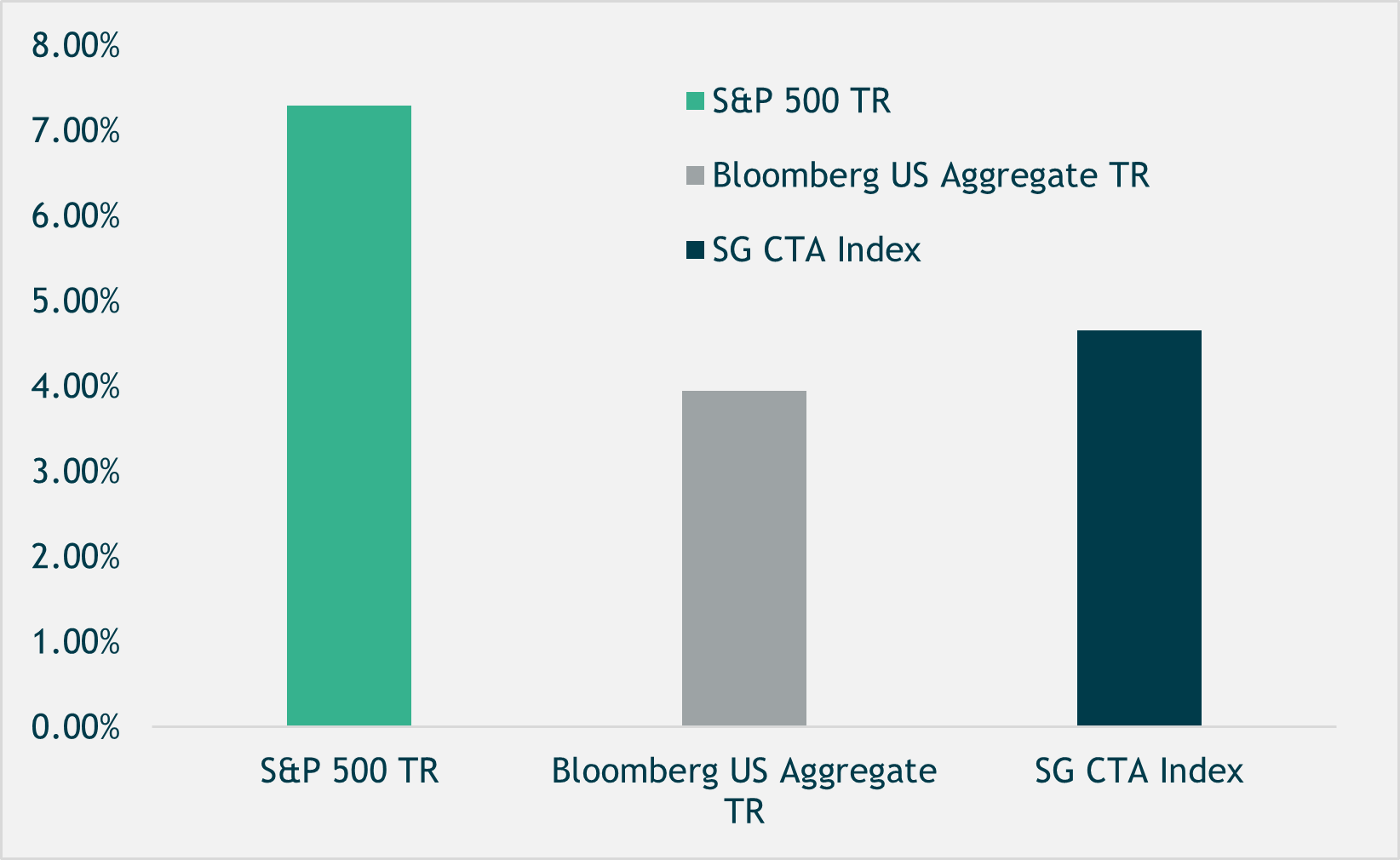

Regardless of the “correct” explanation, over its history, trend following has produced positive returns with essentially zero long-term correlation to traditional asset classes, and has tended to perform best in extended bear markets for stocks and bonds.

DBMF is a simple, cost-effective way to add the benefits of managed futures to a portfolio without the risks of choosing a single manager whose style may be out of sync with markets in any given month, quarter, etc.

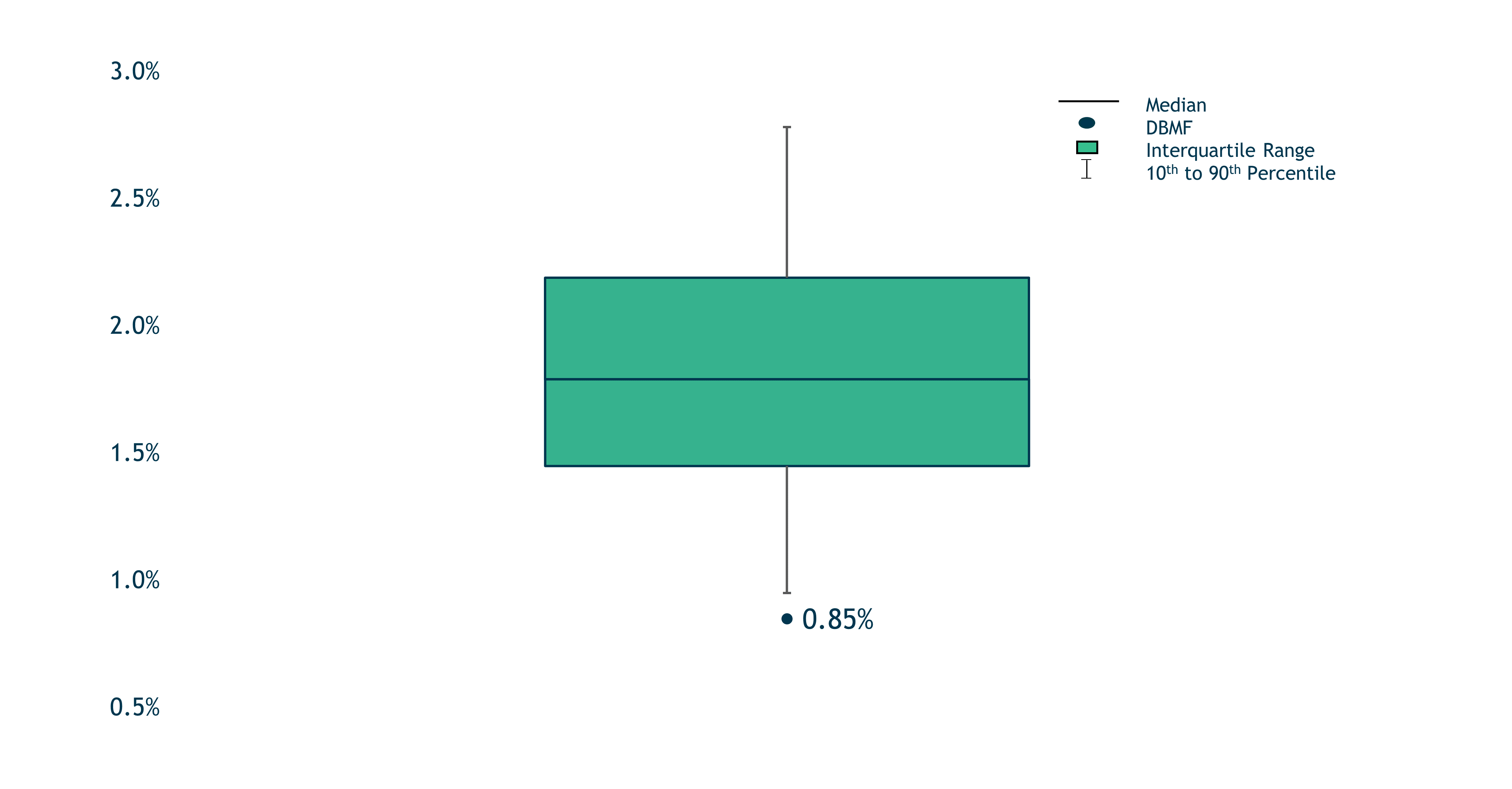

One of the lowest fees in the category

85 bps

DBMF expense ratio is at the bottom decile of peers

Aims to reduce risk of materially underperforming benchmark

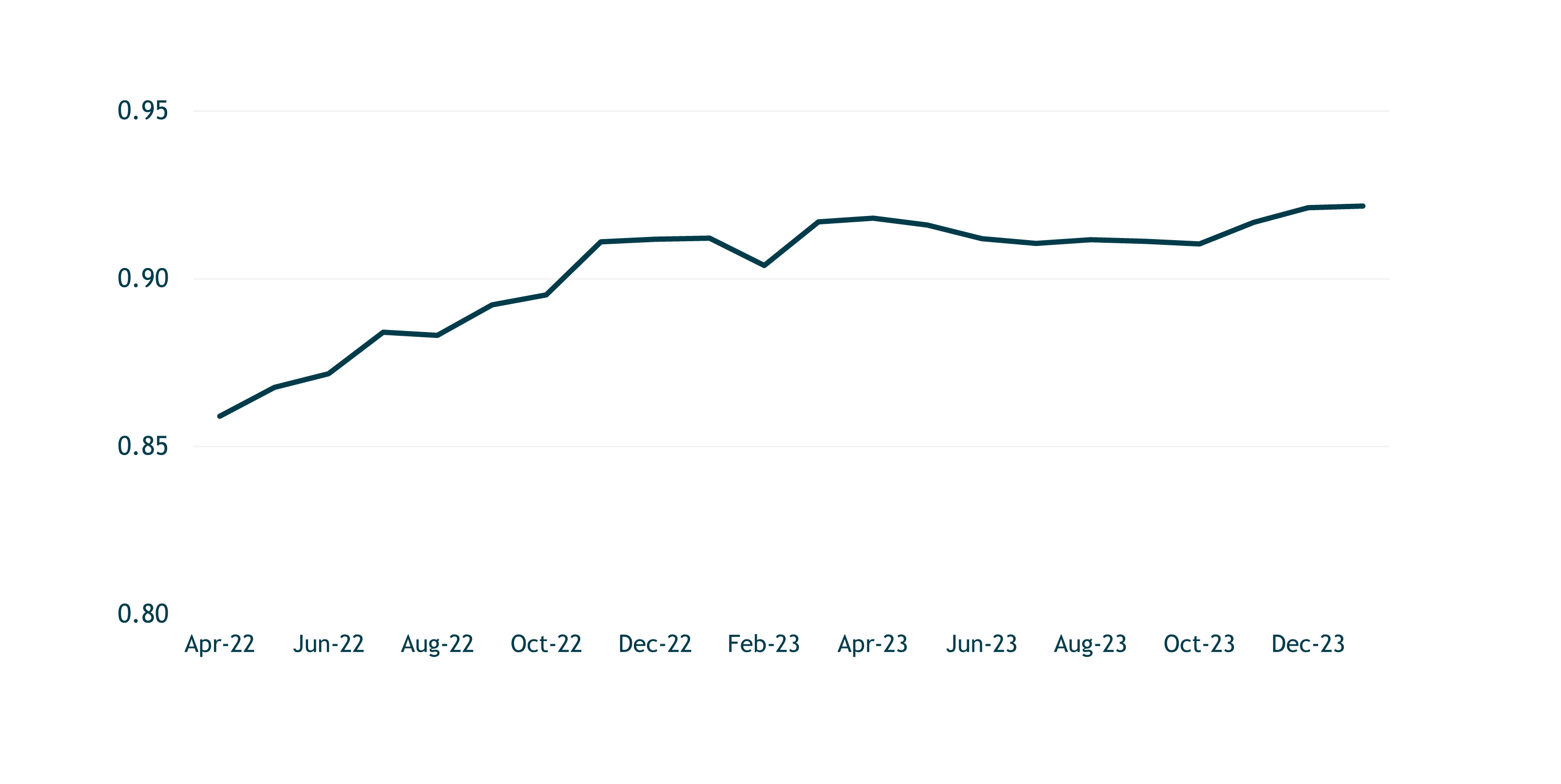

89%

Confidence tracking to index

History of outperforming index

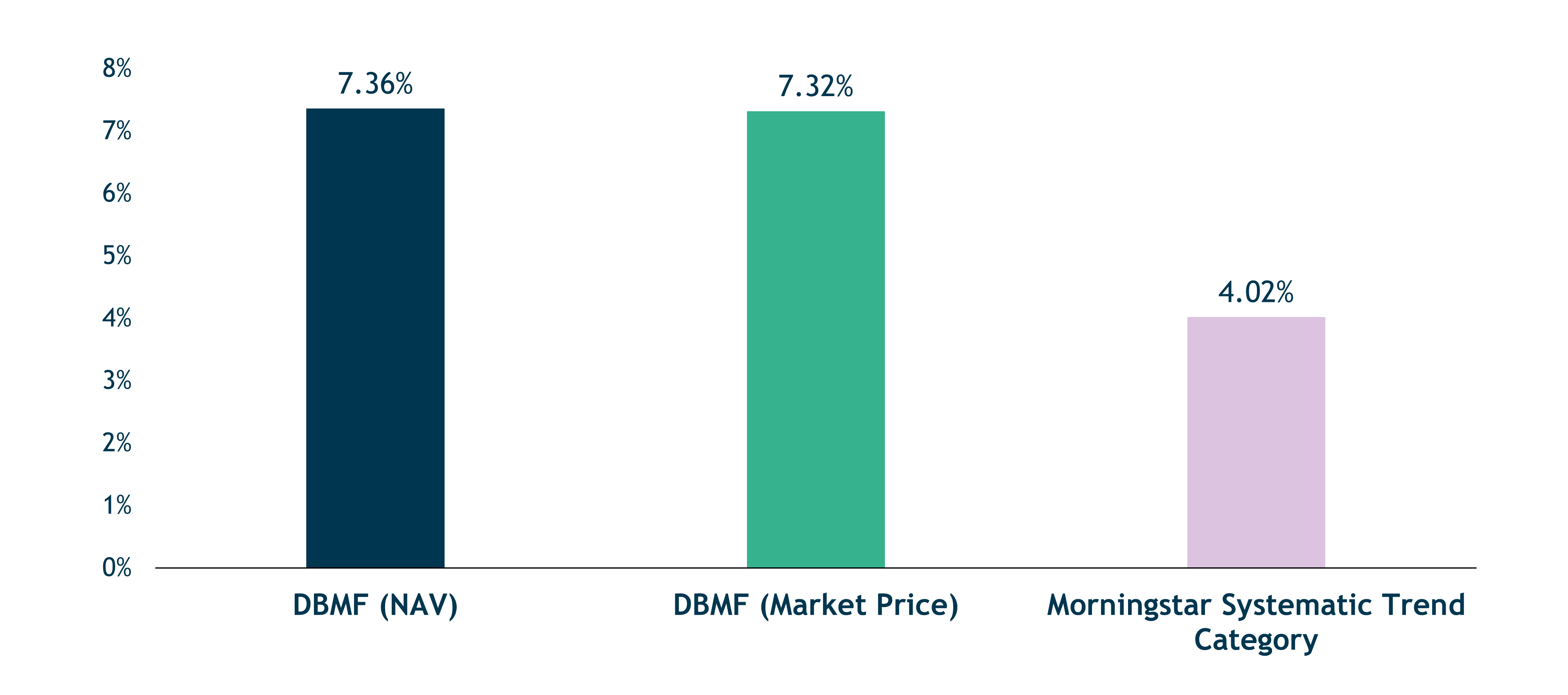

5 years

DBMF has delivered returns over category for 5 years

85 bps

Expense ratio

One of the lowest fees in the Morningstar U.S. systematic Trend category (in the bottom decile of peers - 22 out of 24 funds in the Morningstar U.S. systematic Trend category)

89%

Confidence tracking to index

Aims to reduce risk of materially underperforming benchmark

+1.8%

Excess return (annualized)

Delivered excess returns over its index for the last five years

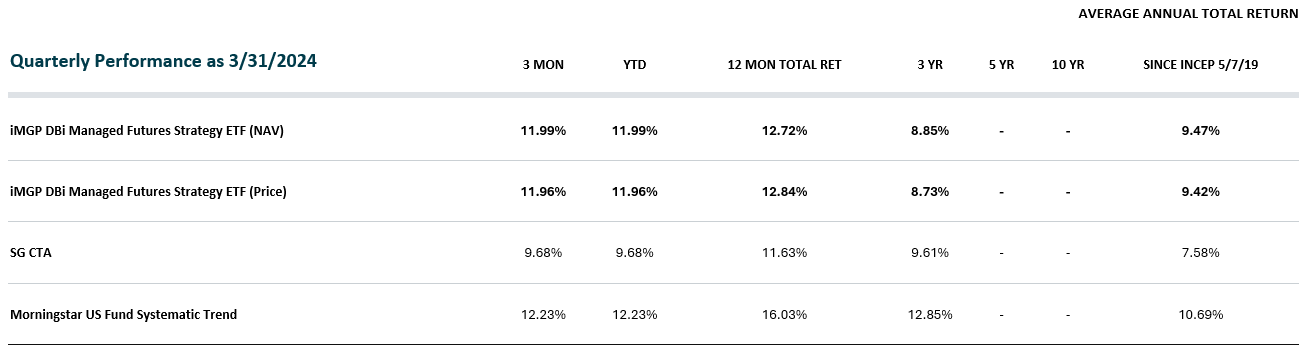

Data as of March 2024

DBI's approach to managed futures

The iMGP DBi Managed Futures fund seeks to replicate the pre-fee performance of a representative basket of leading managed futures hedge funds.

Investment strategy

- The iMGP DBi Managed Futures fund seeks to replicate the pre-fee performance of a representative basket of leading managed futures hedge funds.

- Factor analysis is used to determine the current positions of the managed futures hedge funds.

- The positions are then replicated using highly liquid futures contracts in equity, fixed income, currencies and commodities.

- This approach is a smart and efficient way to gain exposure to managed futures, with the aim of outperforming the representative basket by 300-400 bps per annum, net of fees.

Through this strategy, the fund aims to mitigate three key investment risks:

Market Structure

Illiquidity, trade crowding, counterparty

Concentration

Single Manager, Single fund, industry, geography

Human Biases

Selection bias, etc.

DBI's approach to managed futures

The iMGP DBi Managed Futures fund seeks to replicate the pre-fee performance of a representative basket of leading managed futures hedge funds.

Investment strategy

- Sophisticated multi-factor model analyzes recent pre-fee and pre-trading cost performance of twenty leading Managed Futures hedge funds

- The model determine core long and short factor weights today in key currency, rates, commodity and equity markets

- Exposure built with approximately 15 positions in highly-liquid, exchange-traded futures contracts for efficient execution and maximum liquidity

- Those factor weights typically seek to deliver up to 100% of pre-fee/pre-trading cost returns and most alpha generation over time

- The portfolio is rebalanced weekly, consistent with the rate of change of the underlying portfolios

| Top 5 holdings (as of December 31, 2023) | |

|---|---|

| S&P 500 | 28.3% |

| SOFR | -20.3% |

| 2 Yr Treasury | -20.4% |

| Emerging Markets | -21.0% |

| JPY/USD | -21.5% |

| Asset class exposure (as of December 31, 2023) | |

|---|---|

| US Equities | 28.3% |

| International Developed Equities | 2.6% |

| Commodities | -0.9% |

| Currencies | -13.0% |

| Emerging Market Equities | -21.0% |

| Fixed Income | -58.9% |

DBI's approach to managed futures

The iMGP DBi Managed Futures fund seeks to replicate the pre-fee performance of a representative basket of leading managed futures hedge funds.

- Factor analysis is used to determine the current positions of the managed futures hedge funds.

- The positions are then replicated using highly liquid futures contracts in equity, fixed income, currencies and commodities.

- This approach is a smart and efficient way to gain exposure to managed futures, with the aim of outperforming the representative basket by 300-400 bps per annum, net of fees.

Fee reduction is the purest form of alpha

DBMF seeks to optimize net returns to investors by approximating the main exposures that drive performance, minimizing trading and implementation costs, and offering lower all-in fees.

Hedge Fund

| Continent | Net of fee returns | |

|---|---|---|

| Pre-fee return | ||

| Net return to investors | Management fees, incentive fees & trading costs |

DBMF

| Continent | Net of fee returns | |

|---|---|---|

| Pre-fee return | ||

| Net return to investors | Management fees & trading costs |

DBi's Strategies seek to outperform by delivering 80-100+% of pre-fee hedge fund returns with lower fees and expenses.

DBMF in four minutes

An investment strategy that seeks trends across commodity, rates, currency, and equity markets

See the latest materials from DBMF including factsheets, presentations, commentaries and more

Gross Expense Ratio – 0.85%

Performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 888-898-1041.

Short term performance, in particular, is not a good indication of the fund’s future performance, and an investment should not be made based solely on returns.

All of the assets and liabilities of the Predecessor Fund were transferred to the Fund in a reorganization on 09/20/2021.

Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the Fund. Brokerage commissions will reduce returns.

SG CTA Index:

The SG CTA Index is an index published by Société Générale that is designed to reflect the performance of a pool of Commodity Trading Advisor (CTAs) selected from larger managers that employ systematic managed futures strategies. The index is reconstituted annually.